☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Auditoría de desempeño

Folleto CFH Miami 2013

Peritos y tipos de pruebas

ESAP - Instituto de Administración Pública y Servicios Comunitarios

“Case studies of social and institutional vulnerability: La Boca

Unidades-Análisis-UPLA 040515-R.Reich

Hígado

Pruebas 40/100 G - FelipeReyesVivanco.com

IFLA Mid-Term Congress Case Studies in Government Libraries

Microbiología y Ciencia 2.0 - Biblioteca de la Universidad

Emprendimiento y diseño, la experiencia en HP

What Is Test Security? - Donna Independent School District

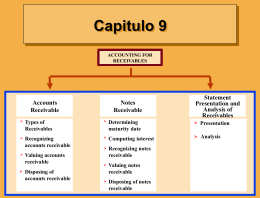

Cuentas por Cobrar Capitulo 9

Detallando planos de AutoCAD

Modelos Econométricos para La ONCE

CR-2010 - Fluid Dynamics Lab Home Page