☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Chapter 9

INFORMATION SYSTEMS AUDIT & CONTROL OVERVIEW

CIS-496 / I.S. Auditing

STRATEGIJA - Valstybės kontrolė

COO’s Office

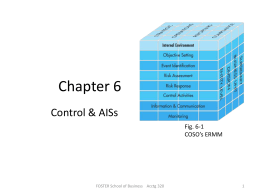

Chapter 6

Slide 1

Security Part 1: Auditing Operating Systems and Networks

Evidencia en auditoría

AIS Development Strategies

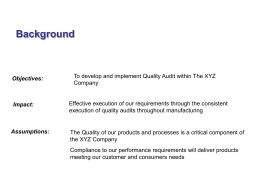

Quality Audits for Manufacturing

ENVIRONMENTAL AUDITING

Crowe Horwath LLP Credentials Toolkit User Guide

Auditor Liability without Regulatory Prescription

1: Introduction

Cartographie des risques - World Customs Organization

Effective Auditing Strategies

Clinical Issues Rising out of Child Welfare Research in

CIS-496 / I.S. Auditing

JJQC Project Management

Mining Charter

Cost Allocation, Customer-Profitability Analysis, and

South African Fruit Growers Ethical Trading Workbook