☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Cost Allocation, Customer-Profitability Analysis, and

Decision Making and Relevant Information

CN03HO

Process Costing

COO’s Office

AIS Development Strategies

Frequently Encountered Families

R.A. Fisher - Evolutionary Biologist

Clinical Issues Rising out of Child Welfare Research in

La Frontera Eficiente de Inversión

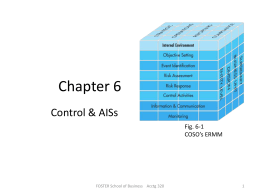

Chapter 6

Culture, Part I

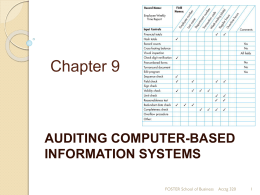

Chapter 9

The Canadian Immigration System: An Overview

Phase 2 introduction - The Global Fund to Fight AIDS

TEVA - NYU Stern - New York University

Loss and Grief for Children in Care