☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

ACCOUNTING & FINANCE FOR BANKERS-JAIIB

jaiib_accfinance_d

The Generations

Chapter 1

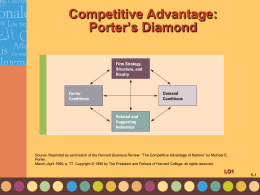

Slide 1

Slide 1

Life Insurance Traps for the Unwary.Larry Herman.121713

Document

Companies Act, 1956 - Force 9! | Positive Thinkers

Slide 1

MILA Marketing FINAL VERSION

Lecture 11 Implementation Issues – Part 2

Relational Calculus - Florida State University

Crucial Paths in Stochastic Modelling for Life Insurers

Slide 1

The Power of the Mandate Sue Hodges Head of …