☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Chapter 1

Chapter 2 - Fisher College of Business

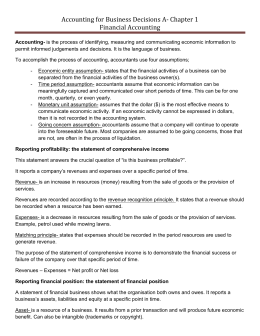

Accounting for Business Decisions A

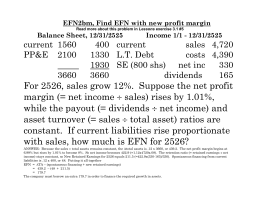

EFN2bm, Find EFN with new profit margin

Chapter 3 - Faculty and Research

Ch 3

Options for Organizing Small and Large Businesses

chapter 18

Chapter 13

Finance and Financing - University of Toronto

CHAPTER 19 Financial Statements for a Corporation

The Generations

chapter 14

Chapter 3: Education That is Multicultural

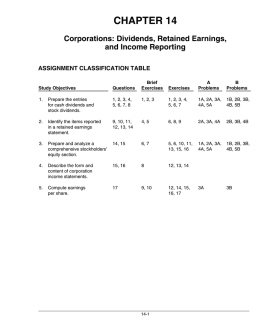

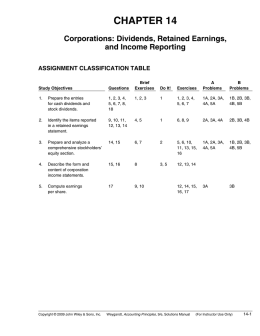

CHAPTER 14 Corporations: Dividends, Retained Earnings, and

Multicultural Education as Equity and Social Justice

St. Michael's Powerpoint template

Document

Introduction to Programming

The Classified Balance Sheet

Minimizing the Administrative Nightmare of Global …

International Equity Markets

Slide 1