☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

You and Your Money - Virginia Guilford

You and Your Money - Virginia Guilford

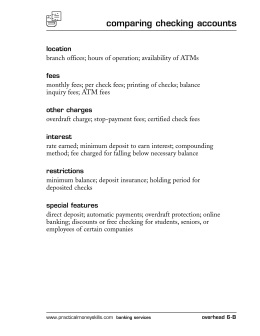

comparing checking accounts

Presentation - Wai Keen Lai

Section 1 a. 10th b. 18 c. Back d. Cashed e. Continental Currency f

Why Should I Have a Budget?

Banking Industry: Structure and Competition - Faculty

Slide 1

An Economic Analysis of Banking Regulation Government safety net

Money and Banking in American History 1833–1933

Future of the Luxembourg Financial Centre

The Evolution of Banking in India

Chapter 9

Pengantar Manajemen Perbankan

Five Forces Shaping the Banking Industry

PDF - World Wide Journals

Organisational change and the computerisation of British and

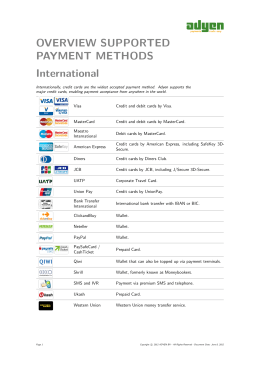

OVERVIEW SUPPORTED PAYMENT METHODS International

Slide 1

Publicity of Deposit Protection Scheme

Trends in Retail Banking Channels: Improving Client Service and

original article in English

Slide 1