☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

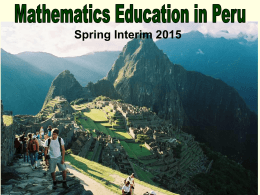

Diapositiva 1

Document

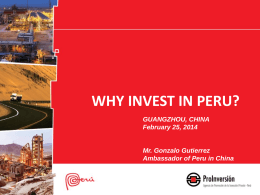

mining investment

Slide 1

Slide 1

Diapositiva 1

Peru - Washington University Bible Fellowship

Family Planning in Peru - University of Pittsburgh

Monetary - Babson College

Portfolios 101 - Carroll County Public Schools

Peru - Santa Ana Unified School District / Overview

Document

מצגת של PowerPoint

Slide 1 by Christina Cerna

Slide 1

Indigenismo and todas las sangres

Andean Civilizations

Catching that elusive butterfly: assessing speaking in