☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Basics of Consumer Protection Law

Pageflex Server [document: 0

Measurements that Matter - CISQ

Welcome & Introductions

assessing fiscal sustainability: a new approach

The CORE Problem Part 2 of X parts

No Slide Title

Learning Objects to Enrich Your Classroom

Document

Slide 1

Northwest Wisconsin Demographic Profile

Towards a multilateral legal framework for debt restructuring: Six

Document

presentation

Recommended Readings: Politics and Community …

The Debt-Equity Trade Off - NYU Stern School of Business

trust - OECD

REGION VII PCCS CONFERENCE– January 2014 Regulatory …

Ministerio de Hacienda

hire purchase - National Debtline

Introduction to Consumer Law” April 8, 2005

Mississippi River Parkway Commission for Grant County

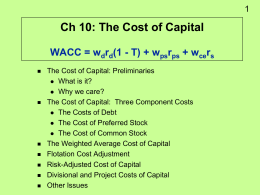

FM10 Chapter 11