☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Project Finance Approach (2)

European Policy Perspective

Rabobank Nederland

Global Virtual Engineering Team Implementation

1 DECC

Sample heading text - Macquarie University

DECC Presentation

Consulation from DECC/EDU on Draft Consequential Order

Joint OHS Committees in the NL Offshore Area - c

Document

Diapositiva 1

Graphplan/SATPlan

Slide 1

Document

advanced epc in the eesi2020 project

Overview of EU R&D on H2/FCs

Survey of Recent Developments at the EPO and in Europe

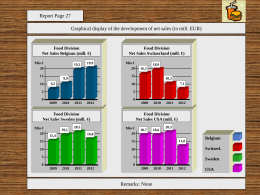

Net Sales - Controller Akademie AG

Presentación de PowerPoint

- Keppel Corporation

Atmel AVR Assembly Language

Chapter 9

Document