☰

Explorar

Iniciar sesión

Crear una nueva cuenta

Pubblicare

×

Descargar

No category

Document

Document

A vehicle for improving government efficiency and …

Understanding Fiscal Policy

Document

Service Oriented Architecture

Press Release-Concluding Statement AIV PPM

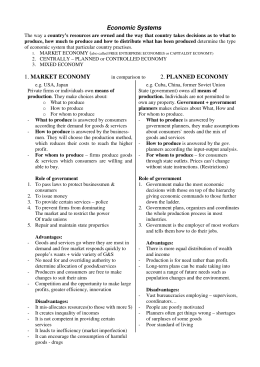

Economic Systems 1. MARKET ECONOMY 2. PLANNED

Document

Figure 15.1 A distributed multimedia system

Présentation PowerPoint - Euro Disney SCA

Distributed Computing - IIT Computer Science Department

Major Initiatives by India to Enhance Transparency in

Document

2016 MVECA USAS FYE Checklist

Fiscal Law Issues in Real Property Transactions

Collecting Data Electronically in Developing Countries

Arkansas Financing Programs

Communicating Bad News

Source of Funds FY 2012 - GSU Finance & Administration

Distributed Computing - Universiti Putra Malaysia

Blocking the FD - CIAT Technology Meeting 2016

Origins of the program